The End of the Innovation Narrative

For years, biomass technologies have been discussed in the language of innovation – pilot plants, breakthrough processes, and future potential. Gasification was “promising.” Pyrolysis was “emerging.” Advanced fuels were “on the horizon.” That phase is over.

What we are now seeing is not a technology race, but a deployment phase. The core conversion pathways are no longer experimental. They are being built, financed, and integrated into industrial systems. The critical shift is: The risk in biomass is no longer technical. It is economic, systemic, and strategic.

The Maturity of Core Conversion Pathways

The main technological routes for biomass conversion are now well established. While incremental improvements continue, the fundamental processes are no longer in question.

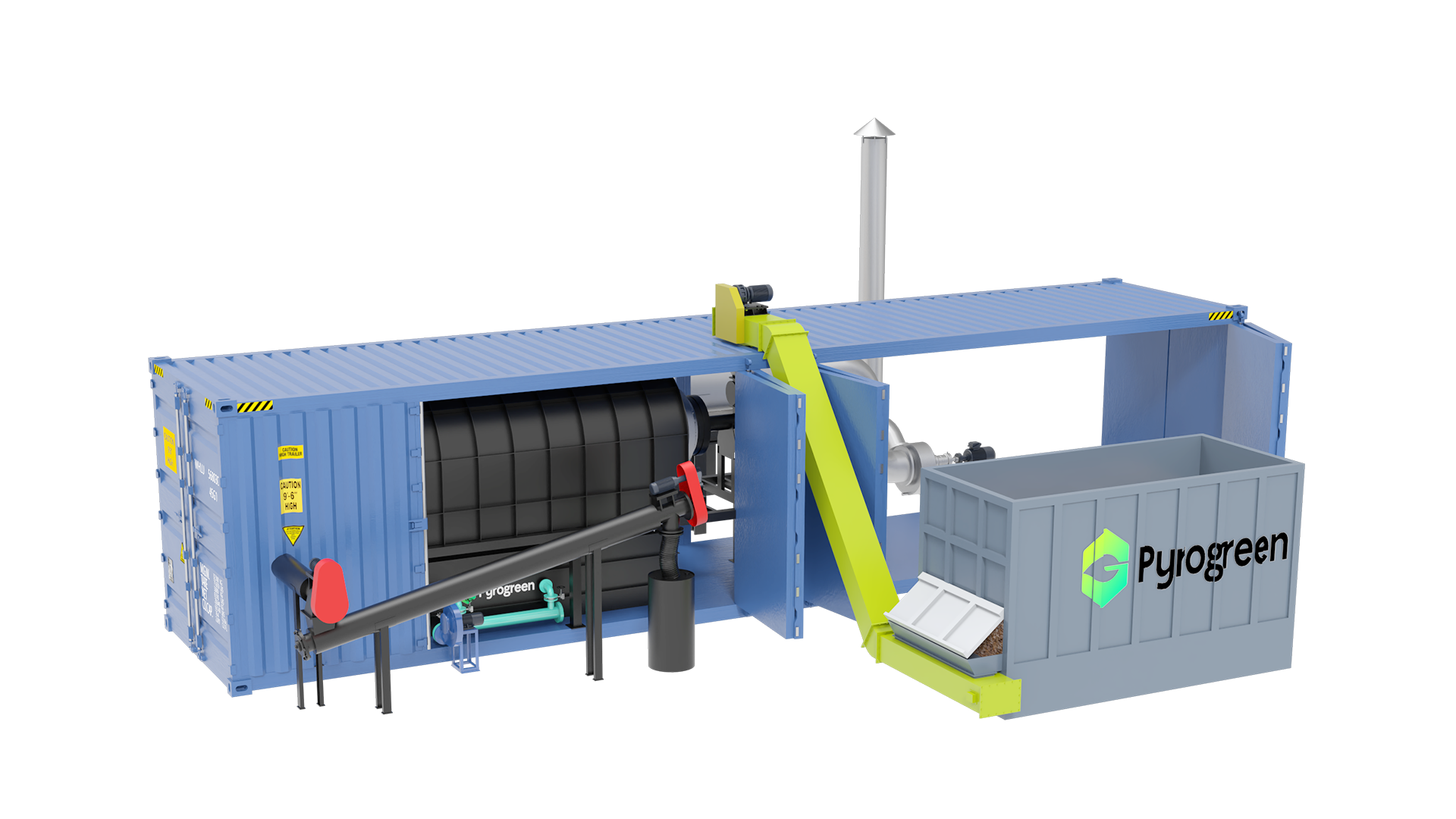

Pyrolysis: From Niche to Platform

Pyrolysis has evolved from small-scale systems into industrial platforms capable of producing biochar (carbon removal), bio-oil (fuel or sequestration pathway), and syngas (energy recovery). Companies like Pyreg and Carbo Culture demonstrate that pyrolysis is no longer experimental—it is modular, scalable, and already deployed. Its real strength lies in flexibility;

energy + carbon removal + material applications in one system.

Gasification: Industrial Backbone for Fuels

Gasification has long been known, but its role is shifting toward high-value fuel production, particularly Sustainable aviation fuel (SAF) and Synthetic fuels via Fischer-Tropsch. This pathway is capital-intensive, but technologically mature. The challenge is no longer “can it work?” – it is: Can it compete economically under current policy frameworks?

Biogas and RNG: Quiet Scaling

Renewable natural gas (RNG) and biogas systems are often overlooked because they lack the “innovation narrative.” But they are among the most deployed biomass technologies globally.

They offer:

- Immediate emissions reductions

- Integration into existing gas infrastructure

- Strong policy support in multiple regions

This is not future tech. It is already scaling at industrial level.

The Conference Signal: From Innovation to Execution

A closer look at the conference agenda shows a clear pattern:

- Fewer discussions about “breakthrough technologies”

- More focus on:

- Project financing

- Commercial deployment

- Supply chain integration

- Policy alignment

This is a classic industry transition. When conversations shift from “what works” to “what scales,” you are no longer in an innovation phase – you are in an execution phase.

The Real Risks: No Longer Technical

If technology is no longer the primary uncertainty, what is?

1. Economic Viability

Many biomass pathways – especially SAF and advanced fuels – are:

- Capital-intensive

- Dependent on policy incentives

- Sensitive to feedstock costs

Without supportive frameworks, even mature technologies struggle to compete with fossil alternatives.

2. Feedstock Dependency

As discussed in Day 2, all technologies converge on the same constraint:

Sustainable biomass supply

Even the best technology fails without reliable feedstock access.

3. Policy and Carbon Accounting

The economics of biomass are increasingly shaped by:

- Carbon intensity scores

- Subsidies and mandates

- Carbon credit systems

For example:

- SAF viability depends heavily on regulatory frameworks

- Biochar depends on carbon credit markets such as Puro.earth

Technology does not determine value anymore – policy does.

4. System Integration

Biomass technologies do not operate in isolation. They must integrate into:

- Energy systems

- Industrial processes

- Supply chains

- Carbon markets

This creates complexity that goes beyond engineering.

The Strategic Shift: From Technology to Positioning

Because the core technologies are now understood, competitive advantage is shifting elsewhere. Winning strategies will be defined by:

- Feedstock control

- Market access (fuels, chemicals, carbon credits)

- Policy alignment

- Geographic positioning

In other words: The winners will not be those with the best technology, but those with the best system integration.

A Misleading Narrative: “We Need Better Technology”

There is still a persistent narrative that biomass needs technological breakthroughs to scale. This is increasingly misleading. The industry does not suffer from a lack of technology. It suffers from misaligned incentives, fragmented markets, and resource constraints. Waiting for “better technology” risks delaying deployment of solutions that already exist.

What This Means for Investors and Industry

For investors, this shift changes the evaluation criteria fundamentally. The key questions are no longer: Is the technology proven?

But:

- Can the project secure feedstock?

- Is it aligned with policy incentives?

- Does it generate multiple value streams?

- Can it compete under realistic market conditions?

For industry players, the implication is clear:

Stop optimizing the reactor.

Start optimizing the system.

Conclusion: The Industry Has Already Moved On

The biomass sector has quietly crossed an important threshold. It is no longer waiting for innovation. It is now dealing with deployment. This shift is easy to miss because it lacks the excitement of new technology announcements. But it is far more important. It means:

- The tools are already available

- The barriers are now structural

- The competition is moving upstream and downstream

The key question is no longer: “Which technology will win?” It is:

“Who can deploy, integrate, and scale what already works?”

Sources

- Biomass Conference & Expo Agenda

https://www.biomassconference.com/ema/DisplayPage.aspx?pageId=Agenda_Biomass_Conference___Expo - Pyreg

https://www.pyreg.de - Carbo Culture

https://www.carboculture.com - Puro.earth

https://puro.earth - International Energy Agency – Bioenergy

https://www.iea.org/reports/bioenergy - IPCC Reports

https://www.ipcc.ch